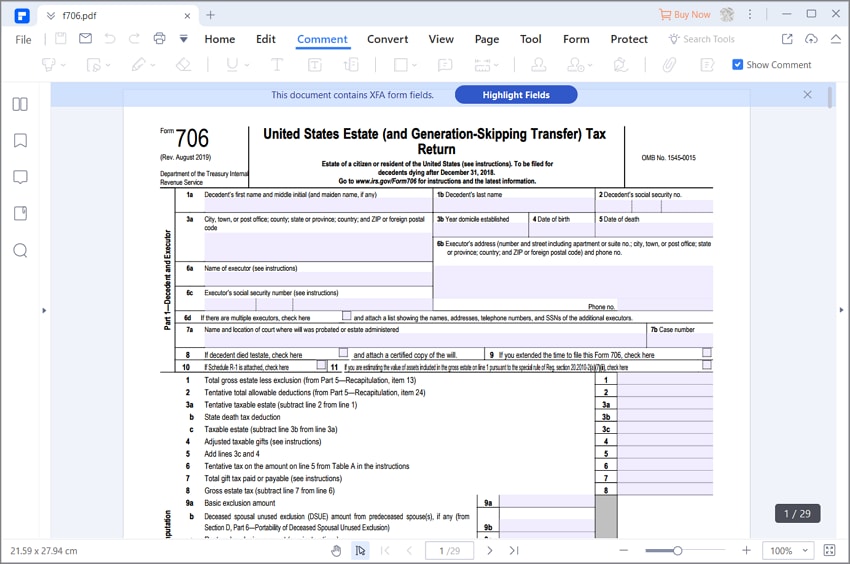

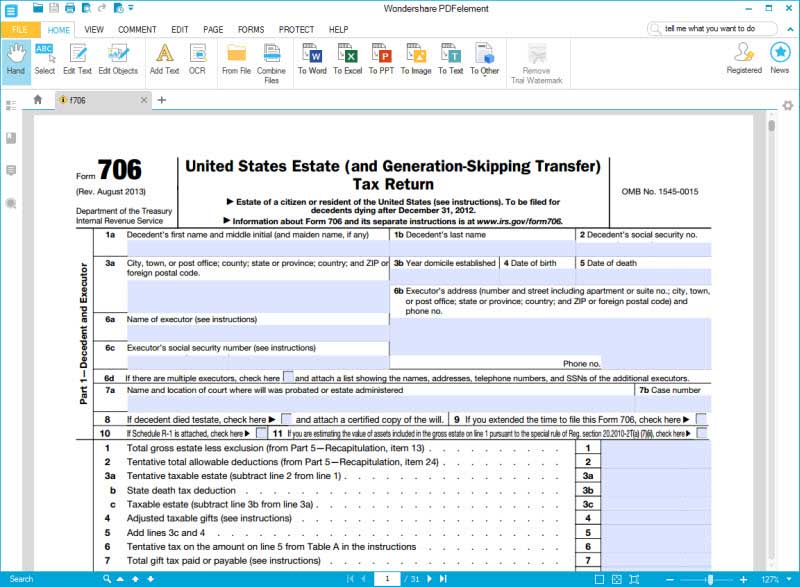

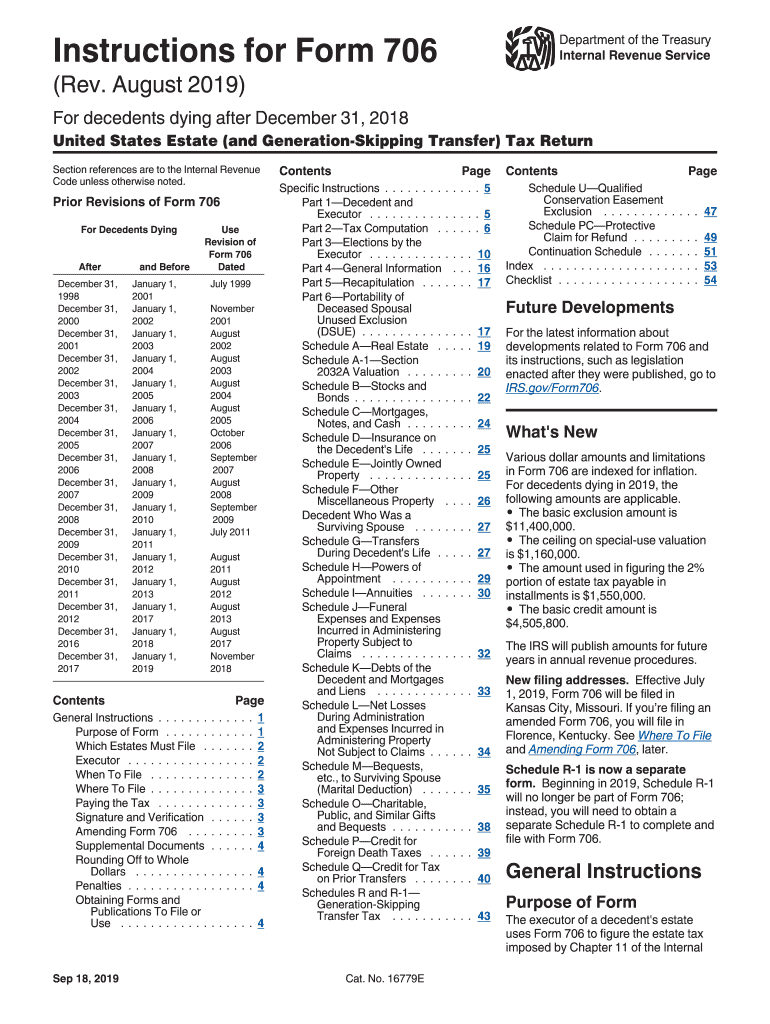

Form 706 Filing Requirements

Form 706 Filing Requirements - Form 706 must be filed by the executor of the estate of every u.s. Information about form 706, united states estate (and generation. You must file form 706 to report estate and/or gst tax within 9 months after the date of the decedent's death. Form 706 is used to figure the estate tax imposed by chapter 11, and compute the gst tax imposed by chapter 13 on direct skips. An estate tax return (form 706) must be filed if the gross estate of the decedent (who is a u.s. Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue). Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. If you are unable to file form 706 by the due date, you may receive. Tax form 706 is required for the decedent’s estate of u.s.

Information about form 706, united states estate (and generation. You must file form 706 to report estate and/or gst tax within 9 months after the date of the decedent's death. An estate tax return (form 706) must be filed if the gross estate of the decedent (who is a u.s. Form 706 is used to figure the estate tax imposed by chapter 11, and compute the gst tax imposed by chapter 13 on direct skips. Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue). If you are unable to file form 706 by the due date, you may receive. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. Tax form 706 is required for the decedent’s estate of u.s. Form 706 must be filed by the executor of the estate of every u.s.

Form 706 must be filed by the executor of the estate of every u.s. Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. An estate tax return (form 706) must be filed if the gross estate of the decedent (who is a u.s. Information about form 706, united states estate (and generation. Form 706 is used to figure the estate tax imposed by chapter 11, and compute the gst tax imposed by chapter 13 on direct skips. If you are unable to file form 706 by the due date, you may receive. Tax form 706 is required for the decedent’s estate of u.s. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue). You must file form 706 to report estate and/or gst tax within 9 months after the date of the decedent's death.

for How to Fill in IRS Form 706

Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue). Tax form 706 is required for the decedent’s estate of u.s. You must file form 706 to report estate and/or gst tax within 9 months after the date of the decedent's death. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. Form.

Instructions for How to Fill in IRS Form 706

Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. If you are unable to file form 706 by the due date, you may receive. Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue). Form 706 is used to figure the estate tax imposed by chapter 11, and compute the gst tax.

Fillable Online Form 706 Na Instructions Fax Email

Form 706 is used to figure the estate tax imposed by chapter 11, and compute the gst tax imposed by chapter 13 on direct skips. You must file form 706 to report estate and/or gst tax within 9 months after the date of the decedent's death. Form 706 must be filed by the executor of the estate of every u.s..

Form 706 Edit, Fill, Sign Online Handypdf

If you are unable to file form 706 by the due date, you may receive. You must file form 706 to report estate and/or gst tax within 9 months after the date of the decedent's death. Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. Information about form 706, united states estate (and.

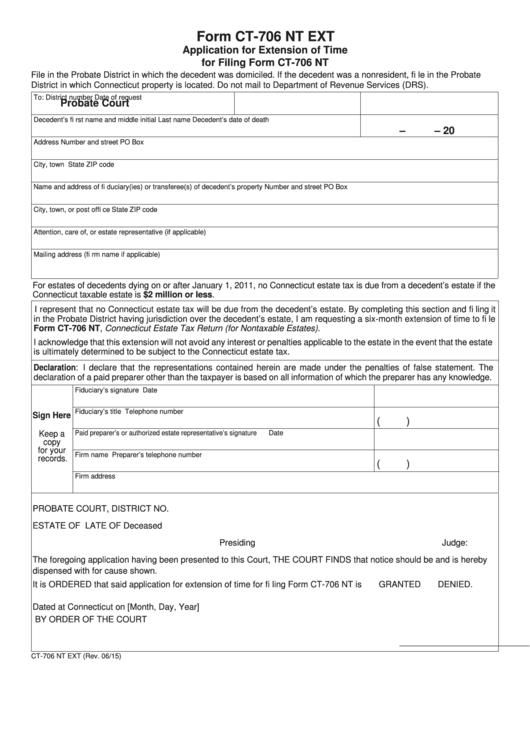

Form Ct706 Nt Ext Application For Extension Of Time For Filing Form

Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue). If you are unable to file form 706 by the due date, you may receive. Tax form 706 is required for the decedent’s estate of u.s. Information about form 706, united states estate (and generation. Form 706 is used to figure the estate tax imposed by chapter 11, and.

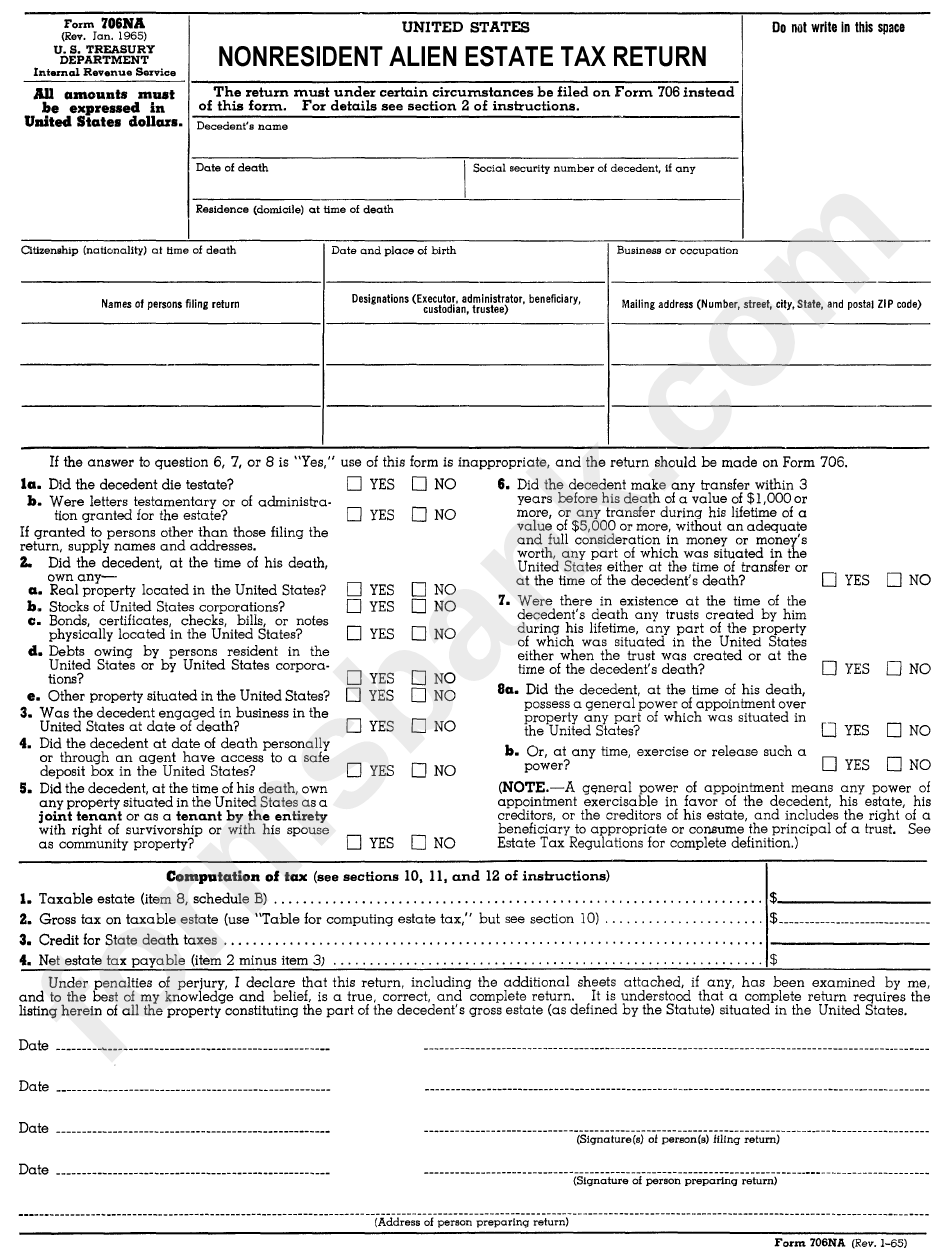

Form 706 Na (Rev. 011965) Nonresident Alien Estate Tax Return

Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue). An estate tax return (form 706) must be filed if the gross estate of the decedent (who is a u.s. You must file form 706 to report estate and/or gst tax within 9.

Fillable 706 2019 Complete with ease airSlate SignNow

Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. If you are unable to file form 706 by the due date, you may receive. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. Form 706 is used to figure the estate tax imposed by chapter 11,.

form 706 instructions 2020 Fill Online, Printable, Fillable Blank

If you are unable to file form 706 by the due date, you may receive. Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. Tax form 706 is required for the decedent’s estate of u.s. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. Whose executor.

Plcb 706 Form ≡ Fill Out Printable PDF Forms Online

Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. If you are unable to file form 706 by the due date, you may receive. Form 706 is used to figure the estate tax imposed by chapter 11, and compute the gst tax imposed by chapter 13 on direct skips. Whose executor elects to.

Form 706 na Fill out & sign online DocHub

Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. An estate tax return (form 706) must be filed if the gross estate of the decedent (who is a u.s. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is. Information about form 706, united states estate (and.

An Estate Tax Return (Form 706) Must Be Filed If The Gross Estate Of The Decedent (Who Is A U.s.

You must file form 706 to report estate and/or gst tax within 9 months after the date of the decedent's death. Tax form 706 is required for the decedent’s estate of u.s. Citizens or residents whose gross estates, plus adjusted taxable gifts and specific exemptions, exceed the federal. Whose executor elects to transfer the “deceased spousal unused exclusion” (dsue).

Form 706 Must Be Filed By The Executor Of The Estate Of Every U.s.

Information about form 706, united states estate (and generation. Form 706 is used to figure the estate tax imposed by chapter 11, and compute the gst tax imposed by chapter 13 on direct skips. If you are unable to file form 706 by the due date, you may receive. Citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is.